All Categories

Featured

Table of Contents

[/image][=video]

[/video]

Roth 401(k) contributions are made with after-tax contributions and then can be accessed (profits and all) tax-free in retired life. 401(k) strategies are created to assist employees and organization owners construct retirement cost savings with tax obligation benefits plus obtain potential employer matching contributions (complimentary added cash).

IUL or term life insurance policy might be a need if you intend to pass cash to heirs and do not believe your retired life savings will certainly fulfill the objectives you have actually specified. This product is intended only as basic info for your convenience and should never be taken as investment or tax suggestions by ShareBuilder 401k.

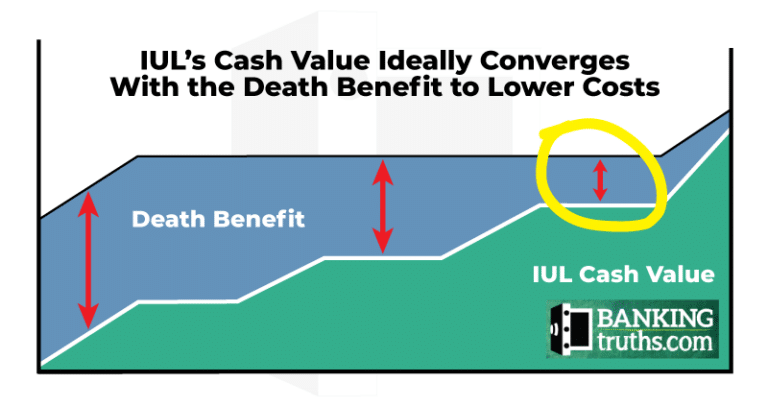

Indexed Universal Life Insurance Versus Life Insurance Policy

If you're searching for life time coverage, indexed global life insurance coverage is one alternative you might want to take into consideration. Like various other irreversible life insurance items, these policies allow you to construct cash worth you can tap during your life time.

That implies you have extra long-term growth possibility than an entire life policy, which uses a set price of return. You also experience extra volatility because your returns aren't assured. Usually, IUL plans stop you from experiencing losses in years when the index declines. They also top your interest credit rating when the index goes up.

Comprehend the benefits and disadvantages of this product to identify whether it aligns with your monetary objectives. As long as you pay the premiums, the plan stays effective for your entire life. You can gather cash money worth you can utilize during your life time for different monetary requirements. You can readjust your premiums and death advantage if your circumstances transform.

Permanent life insurance coverage policies commonly have higher initial costs than term insurance coverage, so it might not be the appropriate option if you're on a tight budget plan. The cap on interest credit scores can limit the upside possibility in years when the supply market performs well. Your policy could gap if you take out as well huge of a withdrawal or plan lending.

With the capacity for more durable returns and adjustable settlements, indexed universal life insurance policy might be an option you want to consider., who can examine your personal scenario and supply tailored understanding.

Iul Reviews

The info and descriptions included right here are not planned to be full summaries of all terms, conditions and exemptions suitable to the items and solutions. The specific insurance protection under any COUNTRY Investors insurance item goes through the terms, problems and exemptions in the actual plans as provided. Products and solutions defined in this web site differ from one state to another and not all products, insurance coverages or services are offered in all states.

If your IUL plan has ample cash worth, you can borrow against it with flexible repayment terms and reduced rate of interest. The option to develop an IUL plan that reflects your certain requirements and circumstance. With an indexed universal life policy, you allocate costs to an Indexed Account, consequently creating a Segment and the 12-month Section Term for that segment starts.

Withdrawals might occur. At the end of the section term, each section earns an Indexed Credit report. The Indexed Debt is computed from the adjustment of the S&P 500 * during that- year duration and goes through the limits proclaimed for that sector. An Indexed Credit is determined for a segment if value stays in the sector at sector maturity.

These limits are identified at the start of the segment term and are ensured for the entire segment term. There are four options of Indexed Accounts (Indexed Account A, B, C, and E) and each has a different kind of limit. Indexed Account A sets a cap on the Indexed Credit score for a section.

The development cap will certainly differ and be reset at the start of a sector term. The participation rate identifies just how much of a rise in the S&P 500's * Index Value puts on sections in Indexed Account B. Greater minimum growth cap than Indexed Account A and an Indexed Account Fee.

Iul Vs Whole Life

There is an Indexed Account Charge related to the Indexed Account Multiplier. No matter which Indexed Account you choose, your cash money worth is constantly shielded from adverse market performance. Money is moved at the very least as soon as per quarter right into an Indexed Account. The day on which that happens is called a move date, and this produces a Section.

At Segment Maturity an Indexed Credit history is determined from the change in the S&P 500 *. The worth in the Segment gains an Indexed Credit history which is computed from an Index Development Rate. That development rate is a percent adjustment in the existing index from the beginning of a Segment up until the Section Maturity day.

Sectors automatically restore for an additional Segment Term unless a transfer is asked for. Premiums obtained considering that the last sweep date and any requested transfers are rolled into the exact same Section to ensure that for any kind of month, there will be a solitary brand-new Segment created for a provided Indexed Account.

Iul

You might not have thought much concerning just how you want to spend your retired life years, though you most likely recognize that you don't want to run out of cash and you would certainly like to keep your current lifestyle. [video: Text appears next to the business man speaking to the camera that reads "company pension", "social security" and "savings".] In the past, people trusted three primary incomes in their retired life: a firm pension plan, Social Protection and whatever they would certainly taken care of to save.

Less employers are supplying conventional pension. And many firms have decreased or ceased their retired life plans. And your capability to rely only on Social Safety remains in inquiry. Also if benefits haven't been reduced by the time you retire, Social Protection alone was never planned to be enough to pay for the way of living you desire and should have.

Index Universal Life Insurance Wiki

While IUL insurance might verify valuable to some, it's essential to comprehend just how it works before buying a plan. There are several advantages and disadvantages in comparison to various other types of life insurance policy. Indexed universal life (IUL) insurance plan provide higher upside prospective, adaptability, and tax-free gains. This type of life insurance policy uses permanent insurance coverage as long as costs are paid.

firms by market capitalization. As the index goes up or down, so does the price of return on the cash money value part of your plan. The insurer that releases the plan may offer a minimal surefire rate of return. There may also be a top limit or rate cap on returns.

Economic professionals typically recommend having life insurance protection that's equal to 10 to 15 times your annual earnings. There are several downsides connected with IUL insurance coverage that critics fast to explain. For example, someone who develops the plan over a time when the market is choking up might wind up with high premium payments that don't add in all to the cash worth.

Besides that, maintain in mind the complying with other factors to consider: Insurer can set involvement prices for exactly how much of the index return you obtain yearly. For instance, let's state the policy has a 70% participation rate. If the index expands by 10%, your money value return would certainly be only 7% (10% x 70%).

On top of that, returns on equity indexes are frequently capped at a maximum quantity. A plan might state your maximum return is 10% annually, no issue how well the index carries out. These restrictions can restrict the real price of return that's credited towards your account every year, despite exactly how well the policy's hidden index carries out.

IUL plans, on the other hand, offer returns based on an index and have variable costs over time.

{kind=link}

Latest Posts

Iul Sales

Single Premium Indexed Universal Life Insurance

A Quick Guide To Understanding Universal Life Insurance